The Cultural Impact of Private Equity Investment

William Johnson

Managing Director

Date published: 25/06/2026

Private Equity ownership reshapes organisations in ways that go well beyond the balance sheet. The operational discipline, accelerated growth targets, and performance management intensity that typically accompany PE investment can deliver meaningful short-term financial gains, but they also carry significant human costs that are frequently underestimated and sometimes ignored entirely.

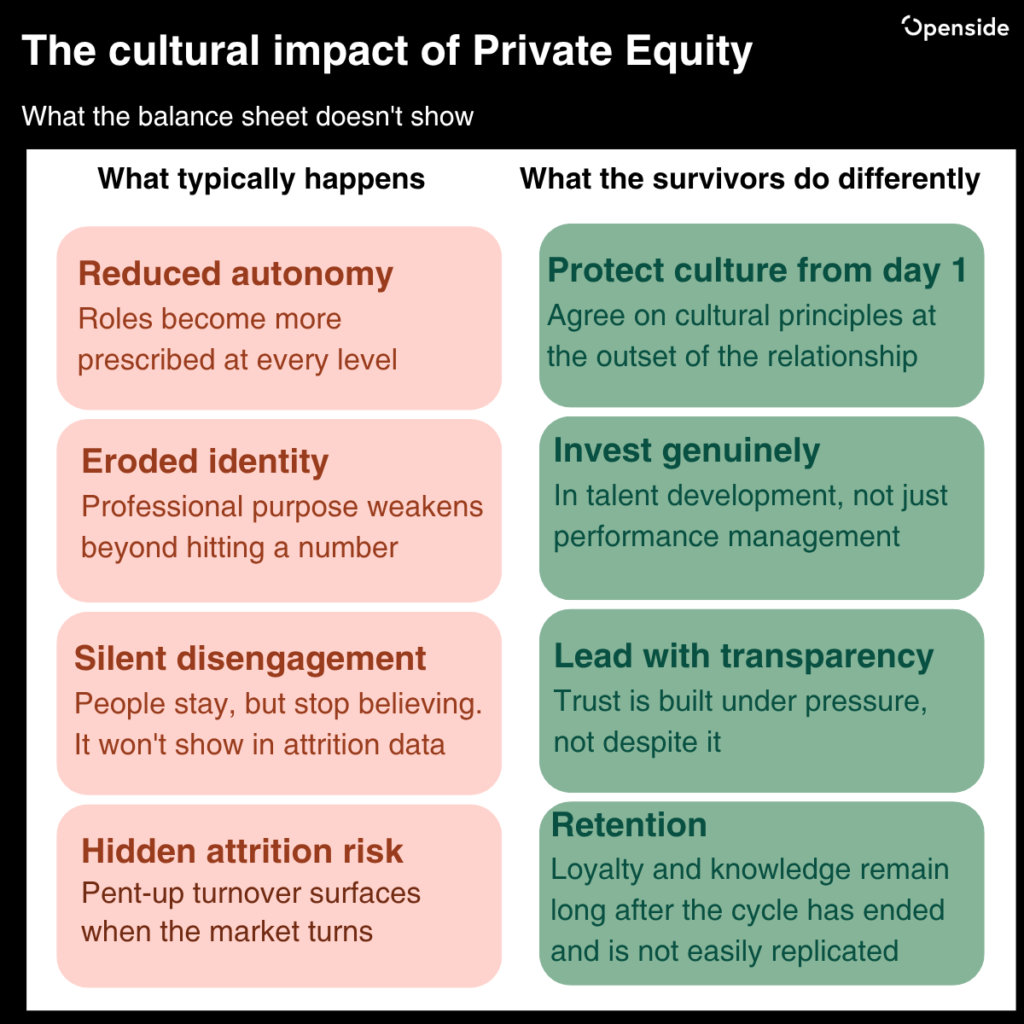

Research on leveraged buyouts points to consistent patterns: reduced autonomy, eroded professional identity, and a weakening of the sense of ownership and purpose that drives discretionary effort. These are not soft concerns. When people no longer feel that their work matters beyond hitting a number, performance eventually follows. The problem is that conventional engagement metrics often fail to capture this deterioration, particularly in constrained labour markets where employees have limited mobility and fewer reasons to signal dissatisfaction openly.

The Human Cost Beneath the Headlines

Our experience indicates that the people impact of the PE model is routinely under-acknowledged – by firms and by investors alike. The push for revenue growth and productivity gains is understandable; it is, after all, the logic of the model. But in practice, it frequently translates into harder work, longer hours, and increasingly prescribed roles at every level below Equity Partner. The flexibility, investment in development, and sense of genuine care that many organisations built their cultures around begin to thin.

What follows is rarely dramatic. It is quieter than that – a gradual accumulation of resentment, a withdrawal of effort that doesn’t show up in attrition data, a workforce that is present but no longer particularly committed. In a tight labour market, people stay. But staying is not the same as engaging, and it is certainly not the same as believing. The pent-up attrition risk this creates is real, and it will surface when conditions allow. The firms that dismiss this as a temporary inconvenience tend to discover otherwise when the market turns.

The Value of Values

The firms that fared best through a PE cycle are those that treated their culture as a strategic asset rather than a casualty of transformation. From the outset of the investment relationship, they secured a clear commitment – not implicit, not aspirational, but agreed – to preserve the principles that made them successful: transparency with their people, genuine investment in talent, and the kind of leadership behaviour that sustains trust under pressure.

This is not an argument against Private Equity. It is an argument for doing it better. Firms that maintain cultural integrity through a PE cycle retain something competitors cannot easily replicate – the loyalty, discretionary effort, and institutional knowledge of people who chose to stay because they still believed in where they worked. That is not a soft outcome. In most professional services businesses, it is the business.